The European Union’s Corporate Sustainability Reporting Directive (CSRD) is driving Environmental, Social and Governance (ESG) reporting across every industry. However, there’s another compelling reason to closely examine CSRD: it introduces a completely innovative ESG reporting framework.

The Corporate Sustainability Reporting Directive (CSRD) serves as the European Commission’s directive for reporting on corporate sustainability matters. Essentially, the EU is urging companies to disclose sustainability risks, opportunities, and management in financial terms. A CSRD report encompasses your company’s approach to various sustainability issues, the financial commitment to mitigate or capitalize on risks and opportunities, and the anticipated outcomes.

CSRD reporting encompasses sustainability comprehensively, addressing all facets of E (environment), S (social), and G (governance). Unlike many other national or market mandates that narrow the scope to disclosures related to climate change and emissions management, CSRD has a broader focus.

In essence, a CSRD report outlines the company’s impact on sustainability throughout the fiscal year, detailing the budget and initiatives for the reporting year and the near future. At the forefront of every CSRD report is the double materiality assessment, analysing how your company influences and is influenced by different sustainability risks.

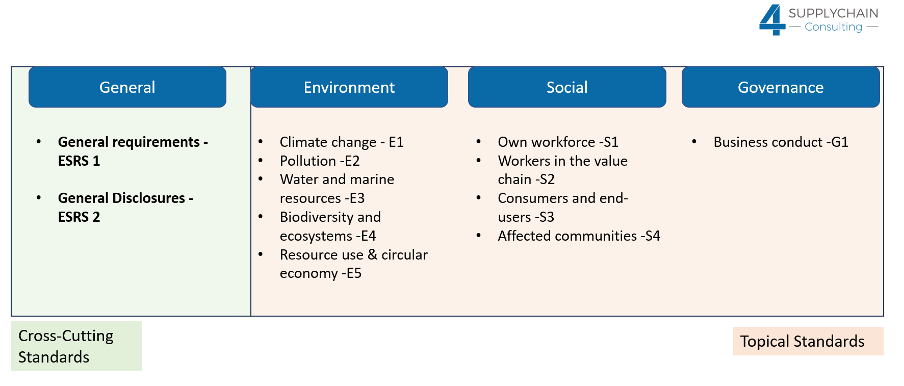

The various sustainability areas are outlined below, each with its own standard developed by the European Financial Reporting Advisory Group (EFRAG). In total, 12 standards were developed:

CSRD distinguishes itself from other national-level mandates but shares similarities with other prominent ESG reporting frameworks.

CSRD takes inspiration from the TCFD framework![]() .It encompasses your company’s oversight of sustainability issues and risk identification, but the core of the report is notably more action-oriented, emphasizing risk management, mitigation, and opportunity initiatives.

.It encompasses your company’s oversight of sustainability issues and risk identification, but the core of the report is notably more action-oriented, emphasizing risk management, mitigation, and opportunity initiatives.

The CSRD Climate Change (E1) section covers all the disclosures recommended in the TCFD guidelines and introduces additional metrics. Notably, ESRS 1, the CSRD standard on General Requirementsmirrors the TCFD architecture. This implies that your CSRD report should go beyond conformity to TCFD and the other national climate disclosures that adhere to the TCFD recommendations.

The Sustainable Finance Disclosure Regulation (SFDR)![]() or the EU Taxonomy, pertains to financial sustainable reporting aimed at financial market participants. In essence, SFRD concentrates on any sustainable investments undertaken by your company, and these activities, classified according to the EU Taxonomy, serve as a supplementary report to CSRD.

or the EU Taxonomy, pertains to financial sustainable reporting aimed at financial market participants. In essence, SFRD concentrates on any sustainable investments undertaken by your company, and these activities, classified according to the EU Taxonomy, serve as a supplementary report to CSRD.

Under SFRD, your company is required to provide details on every activity contributing to an environmentally or socially sustainable objective. If you’re wondering about these objectives, the Commission has comprehensive guidelines.

The EU Taxonomy delineates all sustainable objectives, specifically the six environmental objectives:

Each reported activity must meet the following criteria:

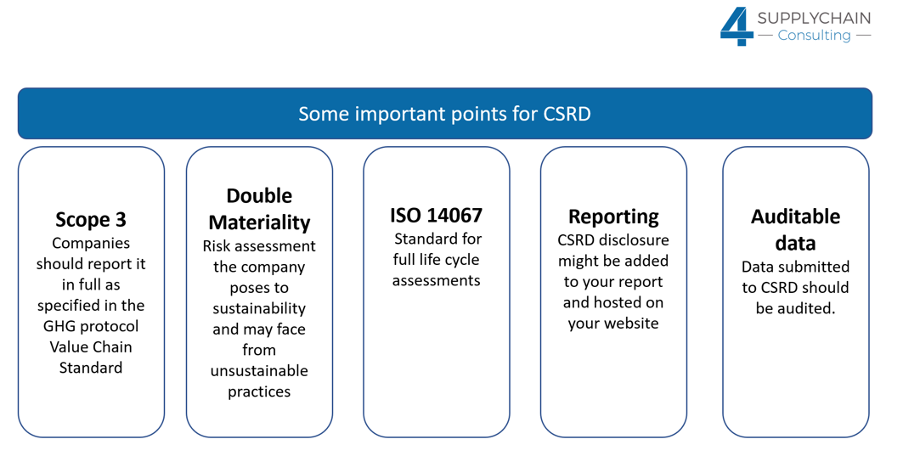

Here’s the curveball: Every reported activity must pass the technical screening criteria, detailed in a 300-page regulation document with a 600-page Annex dedicated to climate change adaptation and mitigation alone. These criteria are based on ISO 14067, the standard for product lifecycle.

CSRD aligns its scope definitions and calculation guidelines for Green House Gases (GHG) emissions under the E1 – Climate Change standard with several key standards from the GHG Protocol, including:

The GHG Protocol Corporate Accounting and Reporting Standard provides requirements and guidance for companies and other organizations preparing a corporate-level GHG emissions inventory.

The Scope 2 Guidance standardizes how corporations measure emissions from purchased or acquired electricity, steam, heat and cooling (called “scope 2 emissions”).

The Product Life Cycle Accounting and Reporting Standard can be used to understand the full life cycle emissions of a product and focus efforts on the greatest GHG reduction opportunities.)

Corporate Value Chain (Scope 3) Standard

The Corporate Value Chain (Scope 3) Accounting and Reporting Standard allows companies to assess their entire value chain emissions impact and identify where to focus reduction activities.)

A notable distinction between CSRD and the GHG Protocol pertains to boundary definitions. While the GHG Protocol considers boundaries outside a company’s financial control as encompassing equity share, financial control, and operational control, CSRD solely defines boundaries based on operational control.

The CSRD reporting standards have been crafted, drawing upon the GRI standard![]() , and as per EFRAG’s assertion

, and as per EFRAG’s assertion![]() , they are completely synchronized. Nevertheless, there are two primary enhancements within CSRD:

, they are completely synchronized. Nevertheless, there are two primary enhancements within CSRD:

While GRI focuses solely on impact materiality![]() , double materiality

, double materiality![]() .

.

While GRI permits the omission of value chain information if unavailable, CSRD mandates value chain reporting and establishes a qualitative standard for data.

In summary, CSRD represents more than just another ESG standard; it signifies a transformation that your company must navigate. However, equipped with the appropriate tools and a resilient strategy, your CSRD report can seamlessly integrate into your regular business operations.

If you require assistance in navigating your CSRD report and data collection, don’t hesitate to reach out to our team of experts!